Neil Birrell, Premier Miton’s Chief Investment Officer and lead manager of the Premier Miton Diversified Fund range, has a look at what is going on in the world of central banks and politicians to impact financial markets at present. As usual, it’s plenty.

For information purposes only. Any views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Investing involves risk. The value of an investment can go down as well as up which means that you could get back less than you originally invested when you come to sell your investment. The value of your investment might not keep up with any rise in the cost of living.

Premier Miton is unable to provide investment, tax or financial planning advice. We recommend that you discuss any investment decisions with a financial adviser.

In brief

- It is a busy month for central bankers with news on interest rates abounding, but we will have to wait for them to be changed.

- Financial markets have remained robust overall, but you need to be in the right parts of them.

- The Chancellor gave his “budget for growth” speech and got us talking about the general election.

Just give us a clue

The day before writing this note, there were interesting things happening in the world of the central banks, which are very worthy of comment.

The European Central Bank (ECB) met and maintained their benchmark deposit interest rate at its all time high level. However, interestingly they did lower their forecast for inflation for this year and next and commented that whilst they were keeping a close eye on the data and were in “no rush” to cut interest rates, they are clearly preparing to do so. Keeping them too high for too long increases the risk of slowing economic growth further and recession.

It was a similar story in the US, where the chair of the Federal Reserve Bank (Fed) said that they were “not far” from having the confidence to reduce interest rates from their 23 year high, as inflation is moving back to the target rate of 2% on a sustainable basis. The Fed meets on 20 March, so we will hear more then.

This is all good news, particularly as investors like certainty and hate uncertainty. This provides more of the former.

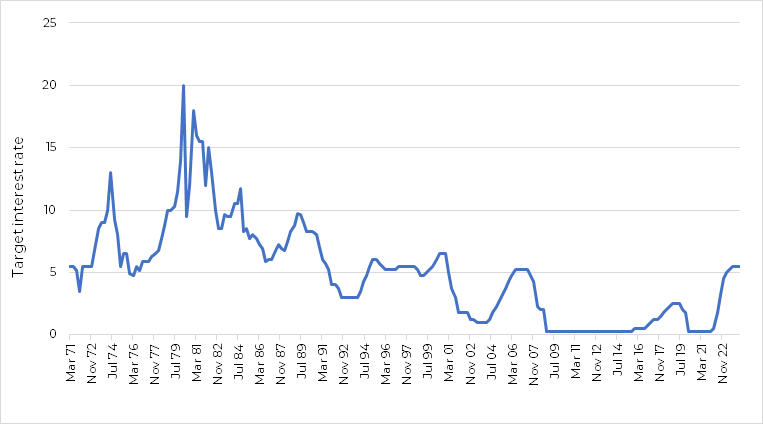

US Federal Funds Target Interest Rate (upper bound) since 1970

Source: Bloomberg 31/03/1971 – 07/03/2024

The Bank of England meets on 21 March. I hope we get similar guidance from them, and as we move towards May and June, the words are put into action.

Has the reality gap closed?

I wrote in January how different financial markets had moved a long way in the hope of early interest rate cuts, but the reality was that those hopes would not be met. It had been expected before Christmas that US rates could start falling this month. As those hopes have waned, markets overall have not really reacted. Bond markets, overall, are a little lower and stock markets (equities) globally are higher. There are differences within those markets and more interest rate sensitive investments have suffered, but it goes to show that investors look to the future, not the present.

However, it will be the scale and speed of the cuts in interest rates that matter and there is still room for disappointment there. However, it looks like we are starting on a journey and interest rates, which stand at levels not seen for a very long time, will soon be falling.

The not so magnificent 7

The Magnificent 7 are the giant US technology and communications companies (Nvidia, Microsoft, Apple, Tesla, Amazon, Google’s parent company Alphabet and Meta, or Facebook) whose share prices had been moving for ever higher, driving US and global stock market indices up and up.

Although the 7 companies were grouped together and talked about as one, they not a homogeneous group of companies and big differences were emerging in how they were being valued; some getting more expensive as their share prices rose and others cheaper. My expectation was that the group would fracture, with the 7 falling to 6, then 5, then 4 etc etc. This in itself presents a risk to stock market indices such as the S&P 500 Index (representing the largest 500 companies in the US) as they have become such a large proportion of it. The same holds true, but in a more diluted form for global indices.

It has been interesting to see what has been happening within the group this year. Nvidia announced its profits for last year and guidance for their sales expectation for this year, the company’s products are key in the explosion of Artificial Intelligence (AI), which sent the share price soaring. Meta (Facebook) announced good profits, cost savings, a first quarterly dividend and a large share repurchase programme; the share price jumped sharply. It is quite possible to argue that their share prices rises are well justified.

Amazon and Microsoft, continue to do well, although their share prices could not be described as cheap and ongoing impressive growth is needed to justify their valuation.

Alphabet (Google), Apple and Tesla, which are very different companies, have been providing less optimistic news, for very different reasons and their share prices have suffered.

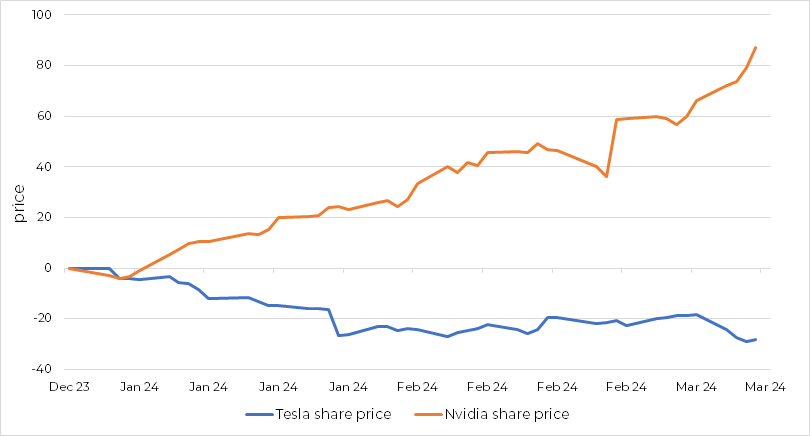

This chart shows how the share prices of Nvidia and Tesla have diverged this year so far, up to 7 March, as you can see it is quite a gap. This is the widest gap between any 2 of the 7, but I am not exaggerating to make the point, it is real.

Tesla and Nvidia share price

Source: Bloomberg 02/01/2024 – 07/03/2024, share prices rebased to 0 on the 02.01.24. The performance information presented on this page relates to the past. Past performance is not a reliable indicator of future returns.

It does look like the band is showing signs of breaking up and in this case, it is hard for me to see it getting back together. As interest rates start to fall, I think it is likely that a company’s fundamentals (such as profits, sales, cash generation and prospects) will take over from macro-economic factors (such as inflation, economic growth and interest rates) in being the main driver of share prices. That should happen not just in the Magnificent 7 but across all regions and company size, making it vital to be exposed to the right companies, not stock markets overall.

To budget or not to budget

The Chancellor provided his “budget for growth” for the UK. The only problem is that the forecasts for growth that accompanied the speech from the Office for Budget

Responsibility (OBR) did not really back that up. The expectations for economic growth this year and next are 0.8% and 1.9%, albeit that is 0.5% more than the forecast last autumn, then between 1.7% and 2.0% looking out to 2028.

These are not economic growth forecasts to get excited about. However, it is growth, not recession and much of the rest of the world is likely to be growing faster than that, which could be a positive impact.

The announcement of a new, additional ISA allowance for specifically UK investments was encouraging. It is something that we, at Premier Miton, have been advocating for some time. It will be good for the UK economy and help restore a thriving stock market, particularly in smaller companies and it will promote investment in the UK. The only problem was that the measures didn’t go far enough. But it was good news. Moreover, the changes to pension fund rules that are being considered could be supportive as well.

Overall, there really isn’t too much to comment on as far as the budget goes, it won’t be long until we are talking about the general election though. Happy days!!