Neil Birrell, Premier Miton’s Chief Investment Officer and manager of the Premier Miton Diversified fund range, looks ahead to 2025 and considers what the New Year might herald for investors.

For information purposes only. Any views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Investing involves risk.

Premier Miton is unable to provide investment, tax or financial planning advice. We recommend that you discuss any investment decisions with a financial adviser. Please refer to the glossary at the end of the document.

Please refer to the glossary at the end of the article.

In brief

- 17 years in brief: how fundamentals have played second fiddle.

- Changing of the guard? What happens next: outlook for US, UK, Europe, China and Japan.

- Three investment opportunities to watch.

17 years in brief: how fundamentals have played second fiddle

There are many, many factors that influence the prices of different assets including bonds, company shares (equities), property, commodities (gold and oil, for example) or more esoteric ones such as Bitcoin and fine art. In the simplest form, it’s demand and supply that drive prices up and down, but there are numerous factors behind those two.

Arguably, since the global financial crisis (GFC) of 2008 / 2009, it has been macroeconomic factors that have dominated in financial assets. These include key trends in interest rates, inflation and economic growth. Virtually every day, all around the world, data is released that relates to macroeconomics. We went through an unprecedented decade of very low interest rates and inflation, with benign economic growth and rising government debt that was exacerbated by the impact of Covid. That was rapidly followed by a spike in interest rates and inflation but not in economic growth.

This has been at the centre of what has driven financial markets. Clearly more specific factors impact as well. In the case of company share prices, what are called fundamentals – their business success, profitability and cash generation – are important, and at times will be the most important. While it is not possible to measure any of this exactly, it does feel like fundamentals have played second fiddle for a long time.

This has led to, and also resulted from, a dramatic increase in investors’ preference for passive investing, in other words buying financial products that replicate indices such as the FTSE 100 Index in the UK or the S&P 500 Index in the US. Investors have moved away from active investing, where a portfolio of individual companies (or other assets) are selected, with the aim of outperforming indices.

Changing of the guard? What happens next

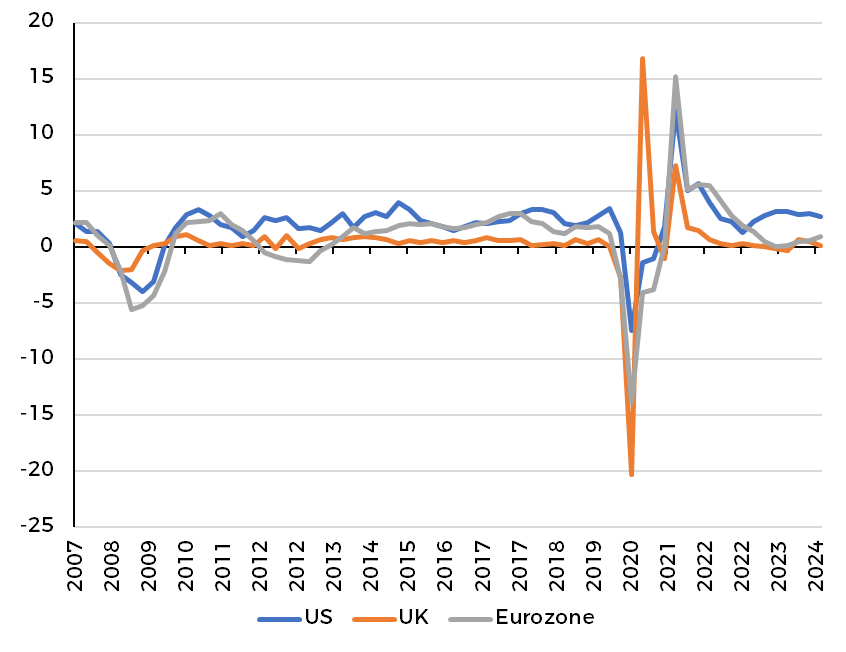

US, UK & Eurozone year-on-year gross domestic product (GDP) growth; 31.12.2007 – 30.09.2024

Source: Bloomberg.

For most of that period much of the world economy has been in sync. This chart shows the economic growth rates (gross domestic product, GDP) of the US, UK and Eurozone since the end of 2007, with the GFC and Covid induced recessions and recoveries clear.

If I was to include China, you would see a similar picture, just with growth at higher levels over that time period. Japan’s GDP also looks similar, but with a lower growth profile.

The key question for all investors is: what happens next? The answer to that may well lie in the big changes we have seen in the political landscape.

US

The unequivocal victory of Donald Trump and the Republican party in the US elections is likely to bring a significant change in US economic policy. The expectation is that it will bring four years of expansionary policy, lower taxes and lighter regulation, resulting in stronger economic growth than was previously anticipated, however, that could be accompanied by increased government debt. Furthermore, if that played out, inflation could remain higher than target, probably just marginally though, and therefore interest rates would probably remain higher as well. However, there is little doubt that the US economy will be getting stimulus from the new administration’s policy measures, which could put it on a faster growth trajectory than other regions. That is, typically, good for equity markets.

UK

In the UK meanwhile, the new government’s policy measures are a long way from providing stimulus to the economy. In fact, in the short to medium term, they are doing the opposite. However, inflation, although much lower now, remains sticky, and therefore interest rate cut expectations have been pared back. Not such a rosy outlook. This could provide a headwind to the equity market, however, it does look cheap by international comparison.

Europe

Europe is in the throes of political change as well, with Germany heading to the polls on 23 February in a snap election after the ruling coalition collapsed and a new one needs to be formed. France is in a political tangle as well, all at a time when the economy is weakening. Eurozone economic growth could lag further.

China and Japan

China recently announced extensive support for its economy, particularly the troubled property sector, which was taken very well and looks positive for its medium-term prospects.

Japan has been through a period of very low economic growth and inflation, both of which they have been trying to encourage through ultra-low, even negative interest rates. With improving economic conditions and changing government policies, those interest rates are on the rise again.

As we go into 2025, political change is leading to fiscal and monetary policy change. This could mean economies around the world de-couple, particularly if US trade tariffs are sizable.

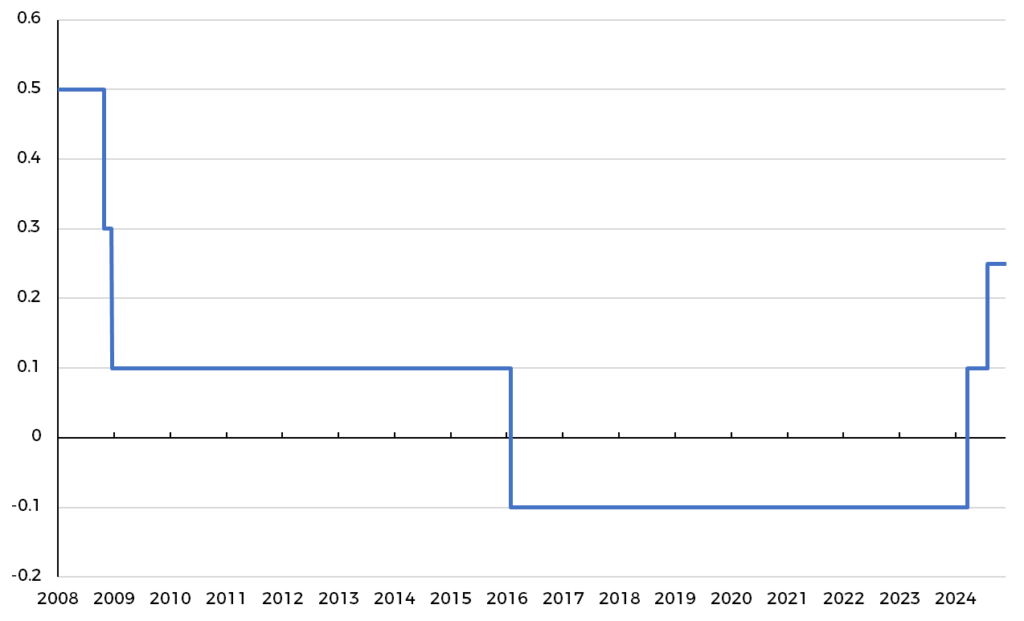

Bank of Japan overnight interest rate; 04.01.2008 – 25.11.2024

Source: Bloomberg.

The reality gap is still here, but maybe it’s not as wide as it was

The difference between what we expect or hope to happen and what actually happens is “the reality gap”. When it comes to interest rate moves, that gap has been wide and constantly changing throughout 2024. At the beginning of the year, with inflation low and economic growth weak, interest rates were expected to fall sharply through the year and into 2025. Now, those expectations have moderated. In the US there are three, maybe four, 0.25% cuts to come by the end of next year. In the UK there are three expected over the next 12 months.

Given the outlook, that seems realistic to me. Therefore, maybe, less room for surprise than we have been used to.

Same old …. macro to win out over fundamentals again next year?

I’m not so sure that will be the case. I may sound like a broken record and may just be disappointed again, but I do feel that we might well be moving towards a phase where asset prices are driven more by specifics relating to them than interest rates and inflation. That’s partly because the of what I’ve outlined above.

The world economy may become less regionally synchronised, and we are moving through a more predictable phase in the interest rate cycle in each region.

That means that investors will be looking for “an edge”, which means that choosing the right balance of assets is vital, which bit of which asset class crucial, and which individual investment could be the key to generating good returns. For example, US companies that are sensitive to a strong domestic economy should do well, whilst large European companies could struggle if US import tariffs are introduced and the local economies stall.

However, in all cases I’d expect the best quality companies to thrive and those that look attractively valued to benefit the most in all regions. Being active in finding them will be the key rather than holding all of them, which is what you do when you invest in a passive fund. I think that the same principle applies to all asset classes; equities, bonds, property and even art!!

Three investment opportunities to watch

It’s a large world, full of different investment opportunities, so I thought I would finish by looking at few of them.

Magnificence

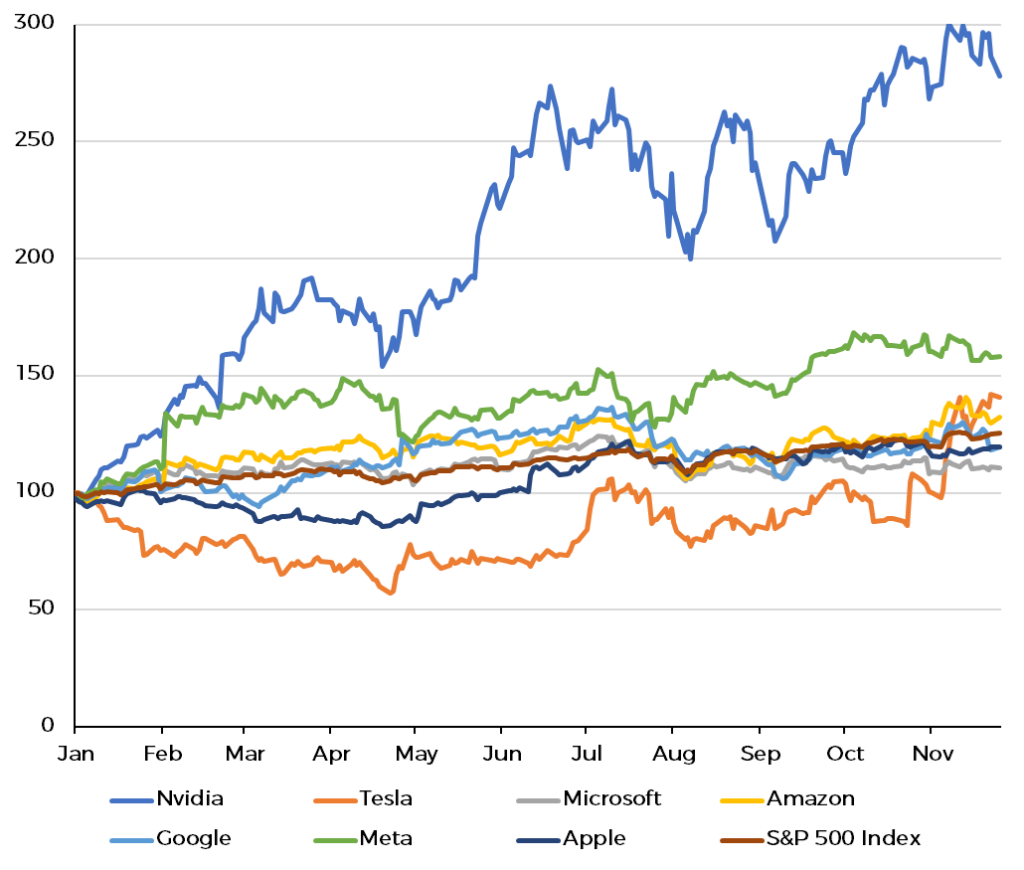

Firstly, the Magnificent 7; Apple, Nvidia, Microsoft, Amazon, Meta (Facebook), Alphabet (Google) and Tesla have been the darlings of the stock market for some time, pushing indices higher. In 2024, up to the time of writing, Nvidia’s share price has surged (up 178%) on the boom and excitement over Artificial Intelligence (AI), whilst Microsoft, Apple and Google are all up by less than the S&P 500 Index, which has risen by 25%. I’d expect the 7 to continue to shrink in number as investors look for value, quality and fundamentals come to the fore.

Percentage gain of the Magnificent 7 and the S&P 500 Index; 29.12.2023 – 25.11.2024

Source: Bloomberg data rebased to 100 as at 29.12.2023. The performance information presented on this page relates to the past. Past performance is not a reliable indicator of future returns.

Talking of AI…

I am no expert whatsoever, but there can be little doubt that we are in the midst of a revolution which can, so far, only be compared to how the arrival of email and the internet changed our lives. That doesn’t mean Nvidia’s share price will carry on up, but we should be prepared for a huge change to society and businesses and investment opportunities available as a result.

Currencies

Foreign currency exchange rates can have a significant impact on the value of your investments, either because the investment itself is quoted in another currency or the currency moves impact on, say, the profitability of a company you hold in Sterling terms. The US Dollar / Sterling exchange rate has ranged from 1.235 to 1.342 this year, while Sterling / Euro started the year at 1.152 and reached nearly 1.21, bouncing around through the year. If we do get regional economies de-coupling, currency moves are likely to remain volatile and high on the agenda.

The last word

An essential part of a fund manager’s job is to manage risks in a portfolio of investments. They can be created by the economic or broad financial market backdrop, they can come from changes to regulations or politics, they can be anticipated or may be a surprise. Nonetheless, it’s crucial to understand the risks and mitigate them, if required, to suit the risk profile of the portfolio being managed and to meet its investment objective.

The type of risk that is very difficult to factor in is that of war or conflict. That can’t be predicted and with the two major ones in Eastern Europe and the Middle East still ongoing, there is the constant threat of a shock to financial markets. We can only hope for resolutions or, at least, de-escalations in 2025 to reduce that risk, but more importantly to reduce the human suffering.