For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Much of the discussion around positioning within multi asset funds is dominated by the equity component. This is understandable, as for many multi asset funds equity is the biggest weight and, more importantly, it is the biggest risk for the vast majority of multi asset funds. Moreover, many funds have little invested in commodities and property, so bonds are the only other asset class to discuss, and bonds, somewhat unjustifiably, still have a boring reputation.

What we have never understood though, is the lack of attention paid to the degree to which the behaviour patterns between all these asset classes change over time. Sometimes two asset classes move in lock step, sometimes they move in opposite directions and sometimes there is no discernible relationship. Importantly, these relationships can and do change. From our perspective, portfolio construction is our most important input and, specifically, we spend a lot of time looking at what is and isn’t working to diversify equity risk.

As our regular readers will know, we have been highlighting for almost two years that equities and bonds will likely be positively correlated. Our view has been, and continues to be, that inflation will be higher for longer and, historically, bonds have not diversified equities when inflation risk is elevated.

As a result, our bond exposure tends to be short duration, which limits exposure to interest rate risk but can provide a very attractive income. For the diversification of equity risk, in an environment dominated by elevated inflation and geopolitical risk, we look to gold, oil and the US dollar.

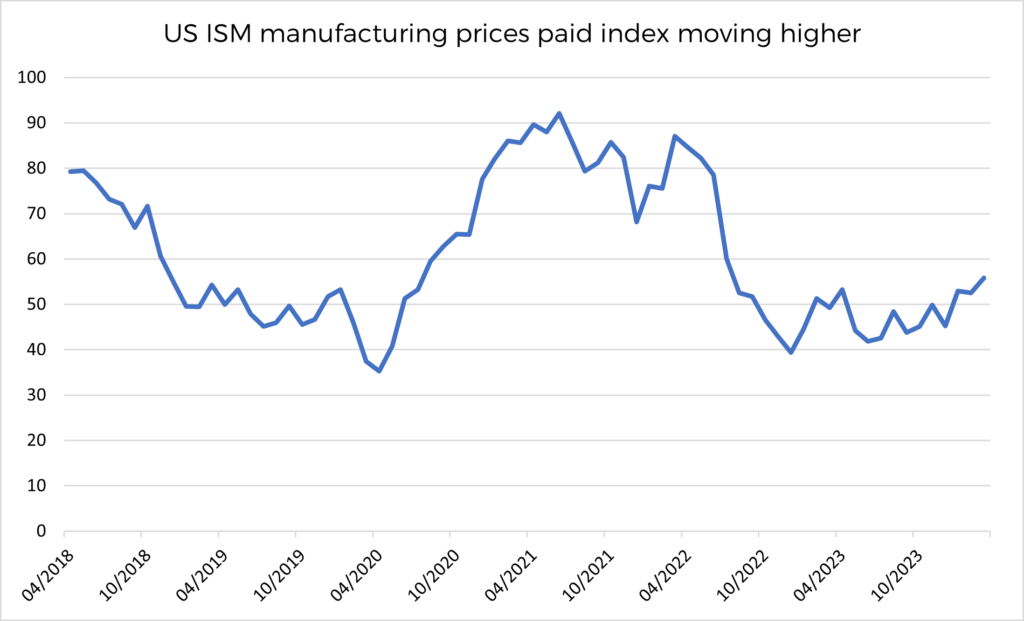

Inflation risk remains a hot topic, fuelled by this week’s ISM prices paid index which was higher than expected, at the highest level since July 2022 and forming a steady uptrend (see graph).

Source: Bloomberg 30.04.2018 – 31.03.2024

Geopolitics also remains a hot topic, with Israel recently targeting the senior command in Iran’s Revolutionary Guard in Syria. How Iran responds will be key, as they, and Hezbollah, have been perceived to be somewhat reluctant to engage, and credibility is everything. Very much related to elevated geopolitical risk, the price of oil is the highest since November and gold is at an all-time high. Similarly, the US dollar has been strong this year, benefiting from the higher for longer trade, with higher US Treasury yields making the US dollar relatively more attractive.

Certainly, developed government bonds have provided little in the way of protection against these elevated risks this year, for example both US Treasuries and Gilts are negative year to date, driven by markets increasingly accepting that rates will be higher for longer.

How asset classes have moved in the first quarter of this year is a good reminder that remaining open minded and considering all the levers available is an important element of managing multi asset funds.

Anthony Rayner

Premier Miton Macro Thematic Multi Asset Team