For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

When we launched our Premier Miton Cautious Monthly Income Fund it was with the pre and post-retirement markets in mind. The most natural way to supply an income need in retirement is from a portfolio that generates income. The efficiency of using income rather than relying on capital gain to fund withdrawal needs is undoubted, even if most clients will need to also withdraw capital from time to time and to maybe achieve additional levels of income if needed.

Prior to the FCA’s Thematic Review of Retirement Income and even more so post the review, we have been having lots of conversations with advisers regarding how to use the fund in a centralised retirement proposition. These have been a fascinating set of meetings, so in this week’s note we thought we would summarise some of the outcomes, and also some of our thoughts regarding the FCA’s paper.

Regarding the Thematic Review of Retirement Income, a few things stood out on the investment front. One was the implication that repurposing a firm’s CIP was considered less than ideal. Another was that how withdrawal rates are determined is in many cases not altogether clear. We think using natural income can help in resolving these two potential regulatory risks, with a further benefit of directly addressing the client’s requirements.

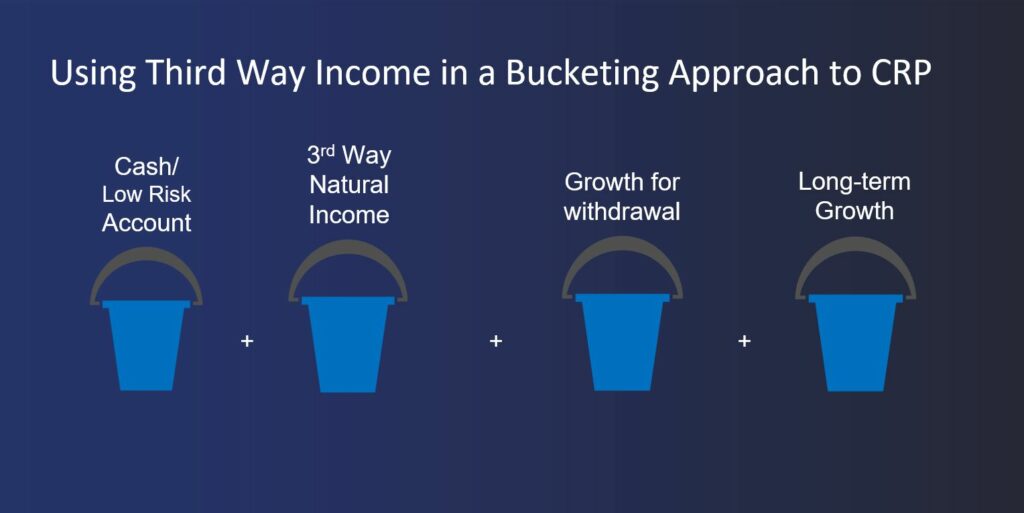

Advisers are becoming increasingly aware of sequencing risk, particularly following the periods of volatility we have seen. Most may understand the beneficial impact natural income can have in mitigating this risk. The difficulty has often been how to implement such a strategy within the confines of an existing ‘on platform’ investment portfolio. The difficulty of implementing a natural income strategy on many platforms has led to the use of unit encashment, even where it is understood to be the riskier strategy. Where clients are using natural income, they often blend natural income with low risk and growth buckets in their centralised retirement proposition in various proportions depending on the end client need.

This bucketing approach seems to be the most intuitive way to deal with the complex problem of post-retirement solutions; by using, typically, three portfolios to meet different needs for the client. The low risk/cash like portfolio is for immediate spending needs and to act as a buffer to redeem from in weaker markets. A natural income portfolio provides for the bulk of spending needs. The long-term growth portfolio provides for legacy, long term spending needs and to be redeemed from in stronger markets. Naturally, the size of these sub-portfolios will be flexed dependent on the individual client’s portfolio and income requirement.

By incorporating natural income into such a CRP, advisers and clients can be confident their income needs are being met irrespective of the ups and downs of markets over time. Of course, the typical client cannot support their full income from natural income alone, but this solid core can be used alongside growth and defensive portfolios to provide the encashment needs. Indeed, the benefits of natural income still apply even if the accumulation shares are bought and redeemed as part of an overall decumulation strategy, that core level of natural income is still being earned.

We think a fund that provides natural income is the obvious core holding in a centralised retirement proposition, the key being to find a true income fund, that manages the income successfully without sacrificing total return. Our investment approach addresses these concerns and we believe it differs from many other dedicated income managers.

David Jane

Premier Miton Macro Thematic Multi Asset Team