Alan Rowsell, Fund Manager of the Premier Miton Global Smaller Companies Fund discusses the past cycles of global small caps and shares why he believes now is the time to look at small caps again.

For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Global small caps have been an excellent asset class for investors, outperforming large caps over the long term. However, their performance is cyclical and the last three years have been tough due to high inflation, rising interest rates and a global economic downturn. We now think we have reached the bottom of the economic cycle and therefore feel the time to revisit small caps is now. Our investment process is starting to flash buy signals in pro-cyclical businesses so a shift in fund positioning from defensives to cyclicals is underway.

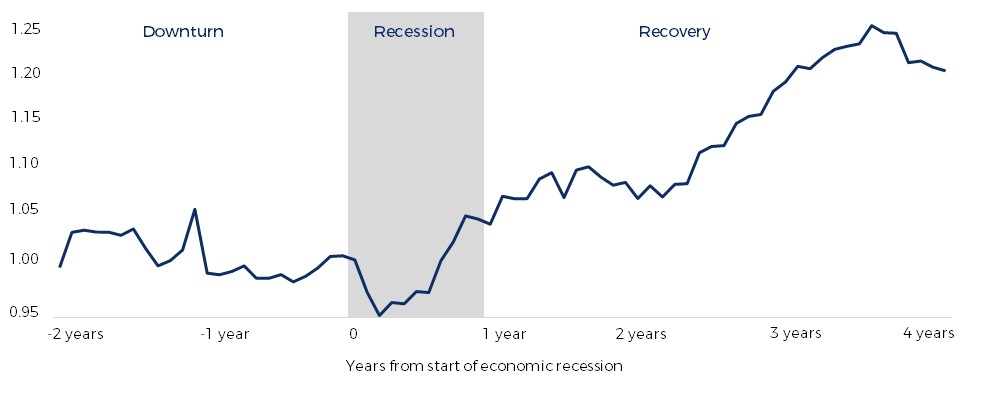

Looking at past cycles, small caps follow a well-defined pattern whereby they tend to underperform going into recessions and outperform coming out. Particularly interesting is that the turn in small cap performance tends to start before the recession is over, i.e. when the news is still bad. The current low for global small caps was in November last year which coincides with an economic recession in the second half of last year in at least thirteen countries, including the UK, Germany, France, Japan and China. As such, this cycle appears to be following the historical playbook which means, in our opinion, now is the time to revisit small caps.

Small caps tend to bottom in recessions – Russell 2000 Index vs S&P 500 Index*

Source: Bloomberg. William Blair Equity Research 1980-2022. *Average relative performance for last 6 recessions starting from 1980 to 2022. Past performance is not a reliable indicator of future returns.

One of the conditions you need for a new bull market is low valuations and three years of underperformance have driven small cap valuations to multi-year lows. For example, forward price-to-earnings multiples for global small caps trade at 14.9x which is the low end of their pre-pandemic range while global large caps trade at 16.9x, the high end of their pre-pandemic range. As a result, the forward price-to-earnings ratio of global small caps relative to that of global large caps has slipped to a 12% discount from an average premium of 18% before 2020. This is the biggest discount since the European sovereign debt crisis in 2011-12 and suggests sentiment towards small caps is rock bottom. It also sets up the potential for significant outperformance as the cycle turns up. With increasing conviction that we have reached the bottom of the economic cycle, are there any signs of economic greenshoots emerging? The answer is yes. Leading economic indicators such as purchasing managers’ surveys have stabilized and, in some cases, started to turn up.

Small cap relative valuation at 10+ year low

Source: Bloomberg. data from 31.01.2014 to 31.01.2024. Past performance is not a reliable indicator of future returns.

Export data in Korea and Taiwan have turned positive. Consumer confidence in many countries is improving, as are house prices. Bank lending standards in the US are beginning to improve and demand for air freight has exceeded capacity growth for the first time in two years.

At the corporate level, companies in cyclical sectors like semiconductors and chemicals are saying the headwind of inventory destocking is abating which means revenues are starting to bounce back. European banks are delivering profit growth again and returning cash to shareholders. Even Greek banks! Biotech funding is starting to increase while hospitals are performing more medical procedures as the labour shortage eases. There is a boom in construction spending in the US as AI drives investment in data centres and national security demands a reshoring of critical industries like semiconductor fabrication. Even the consumer is starting to recover from the cost of living crisis as wage growth begins to exceed inflation. These are just some of the examples of better newsflow that we are seeing.

Our focus has shifted from capital preservation mode to identifying the winners of the new upcycle. To do this successfully, you need a disciplined investment process that screens the entire global small cap universe for companies seeing improving earnings momentum. This means we look for companies delivering positive earnings revisions, where profits are beating consensus expectations. As such, this is neither a growth nor value approach, but instead a pragmatic one that invests in companies where profits and cashflows are getting better and surprising to the upside.

A global approach to small cap investing, as compared to a regional one, offers a wider opportunity set putting us in a better position to identify new trends wherever they emerge around the world. Such an example would be artificial intelligence which has been the big investment theme of the last year. In large caps, it was Nvidia, a US company, that grabbed all the headlines and rose 246% in 2023 to become one of the so-called Magnificent 7 stocks. However, our global small cap screening tool flagged up another beneficiary of the AI boom, a semiconductor design company in Taiwan called Alchip Technologies. It rose by 283% in 2023, outperforming Nvidia, but did not get nearly as much attention!

This is an exciting time for global small caps and our investment process. The last two years have seen several bear market rallies that were not supported by the fundamentals. That has changed in recent months with both positive signals at the macro level being supported by improving earnings prospects at the micro level. That is why we believe now is the time to revisit global small caps and why we are pivoting from defence to offence in the fund.