For information purposes only. The views and opinions expressed here are those of the author at the time of writing and can change; they may not represent the views of Premier Miton and should not be taken as statements of fact, nor should they be relied upon for making investment decisions.

Trends often persist for much longer than investors think, and not just at a market level. It can be a range of dynamics, including geopolitical conflict as well as within the macro environment.

For example, the Fed famously declared inflation was going to be transitory in 2021, only to reverse that view a short period later, once it was clear that they were wrong. Inflation then fell back towards 2%, encouraging markets to assume that it would obediently stay there, i.e. that inflation would be relatively transitory after all.

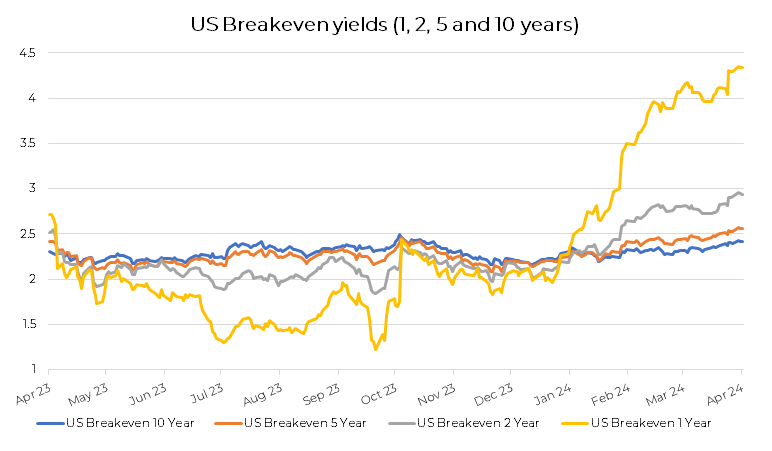

However, the combination of elevated services inflation and a higher oil price has forced investors to renege on the ‘relatively transitory’ view too, and more recently to start pricing in a higher for longer scenario. The chart below shows how the market has rowed back from its optimistic view on US inflation expectations, with the one year breakeven going from 2% at the beginning of the year, to 4.3% now.

Source: Bloomberg Finance L.P – 16/04/2023 – 16/04/202

Looking at another example, but staying in the macro world, there was a strong consensus last year that the US was heading for a recession, due in part to higher rates but also due to a sense that the expansionary stage of the cycle had become over extended. However, just like inflation, and of course they are very related, US growth turned out to be more persistent too.

If we look beyond the macro, the other major story for markets over recent months has been that of geopolitical risk, initially the Ukraine/Russia conflict and then the Israel/Palestine conflict. Both have surprised many in their persistency. Many investors in the West tended to get caught up in their own propaganda and believed Putin’s days were numbered, whether due to internal or external threat.

Turning to the Middle East, many were surprised by the degree of Israel’s response to the Hamas attack and then, forward winding to today, recent actions taken by Israel and Iran suggest that the risk of a regional conflict is increasing. So, again, more persistent than anticipated.

We correctly thought inflation would be higher for longer. We have shared this view with our investors on a number of occasions and have positioned portfolios accordingly, with short duration bonds and a decent exposure to commodities. We were surprised by the persistency of the US economy but never had overly defensive positions in the portfolio, as the signs of a recession never came through in a concrete enough fashion.

In terms of the elevated and persistent conflict in Ukraine and the Middle East, from the beginning we didn’t have a strong view either way, recognising the missive that “truth is often the first casualty in war”.

Therefore, our focus has been on the inflationary environment, where we tend to have a stronger view. Due to the location of the conflicts, and their persistency, they are an additional force feeding into higher inflation. Geopolitical risk is driving the oil price and the gold price higher. In turn, the oil price is driving inflation higher, which in turn is driving the gold price higher.

From a portfolio construction perspective, at times when elevated inflation is a key risk, bonds have historically not helped diversify equity risk. As a result, and in line with our view that we are in a higher for longer environment, we have held commodities to diversify equity risk, and held short dated bonds for attractive income. This remains an appropriate portfolio construction, with long dated developed government bonds losing money year to date and generally not diversifying equity in sell-offs.

Anthony Rayner

Premier Miton Macro Thematic Multi Asset Team